Everything We Were Told About the $175 Million Bond Donald Trump Got Was a Lie

Here’s the truth—which breaking news reports revealed to America over just the last 72 hours.

This report is free. To gain instant access to the other reports in the “Trump Bond Crisis” series—all listed in a Bibliography below—as well as 275+ more Proof reports, just click this button:

Introduction

Across nine sprawling reports—see the Bibliography below in this Introduction—Proof has provided comprehensive coverage of the Trump Bond Crisis in the United States, on several occasions breaking news on this national security-implicating topic that subsequently appeared in major media. We’re now at a stage of the scandal Proof has denominated the Trump Bond War, as law enforcement in the State of New York is contesting Donald Trump’s irregular bonding practices, and the consequences for the 2024 Republican Party presidential nominee could be both financial and political.

If Trump’s bond from Knight Specialty Insurance Company (under the guidance of CEO Don Hankey) is found to be legally or financially insufficient at a “show cause hearing” to be held before Judge Arthur Engoron on April 22, it’s likely that Trump will have no choice but to stand and watch as New York Attorney General Letitia James (who Trump regularly compares to an animal and smears with racist monikers) starts dismantling his real estate empire almost immediately—perhaps even within 24 hours of such a judgment.

ABOVE: Don Hankey, Chair of Knight Insurance Group, headquartered in Los Angeles, CA.

Don Hankey’s ring of lending operations has been called the Trump Family’s “lender of last resort” by Rolling Stone, so if Hankey and the so-called “Knight Bond” are ruled ineligible in the Trump Family/Trump Organization civil fraud case it could mean both the end of Trump’s appeal in the case and the beginning of a stage in his decades-long history of corporate graft with which he has almost no experience: accountability.

Each day, more details are revealed not only about the myriad ways in which the Knight Bond is insufficient or potentially corrupt—even as it’s undoubtedly irregular (see the nine reports in the Bibliography below)—but also about the history between Hankey and his lending institutions and the Trump Family, including Jared Kushner.

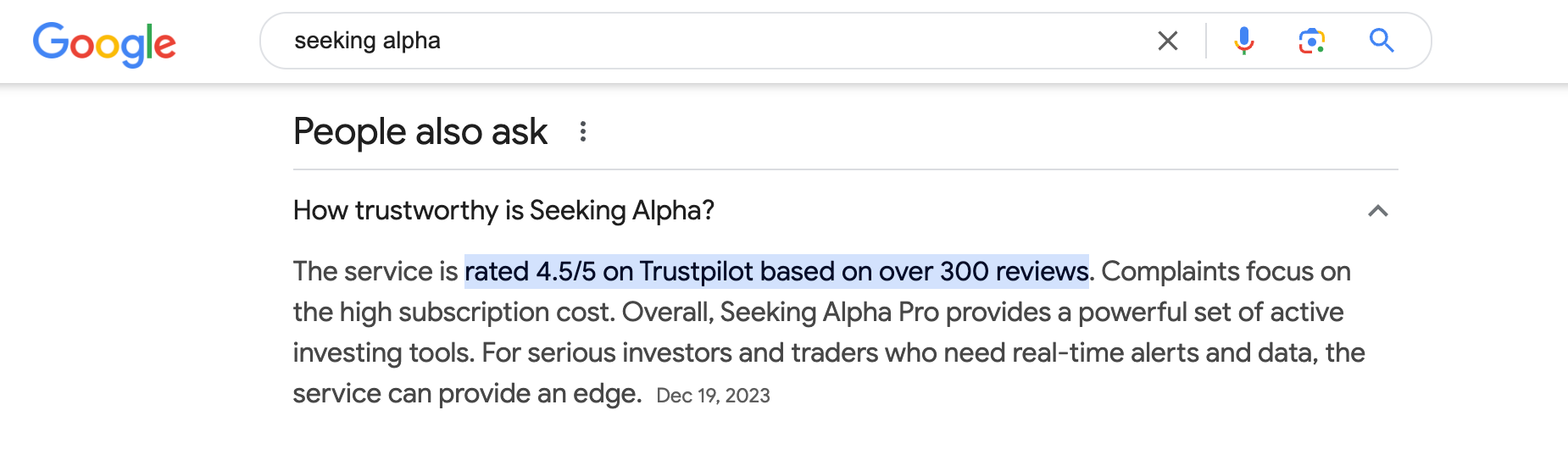

For instance, almost no American news consumers will yet have seen this 2016 report on Seeking Alpha about BOFI (Axos Bank), whose largest investor is Trump’s newest lender (Hankey), which bank has repeatedly lent money to the Trump Family to the tune of hundreds of millions of dollars in the last decade.

While Proof does not often—in fact, almost never—cites anonymous reports, in this case (a) all of the research in the report is from public records, so it can be confirmed; (b) the research contains an appropriate conflict-of-interest disclaimer at its close; (c) Seeking Alpha is a financial services company and crowd-sourced content service that is ranked highly by reliable trust metrics (see image below); (d) the information in the report largely echoes both of the two known Axos federal whistleblower accounts—including that of Charles Matthew Erhart—discussed at length in this ongoing Proof report series; (e) the report was published in 2016, so it’s not merely a convenient reply or reaction to the Trump Bond Crisis and/or Trump Bond War; (f) Proof can find no evidence that its public-record submissions have since been contradicted or disputed; (g) it appears on a well-known and highly regarded platform that regularly—and for readily understandable reasons—publishes anonymous content from evident experts who nevertheless must disclose their potential biases (e.g., the report linked to above is from someone who is “short BOFI” by their own admission, albeit they’re shorting for the reasons outlined in the report); (h) a number of the contentions in the report have subsequently been confirmed by major media, for instance in this Rolling Stone report and other major-media reports linked to by Proof in this ongoing series (see the Bibliography below); and (i) the purpose in Proof posting the information below is to encourage major-media journalists working on the Trump Bond Crisis and Trump Bond War to do more investigative journalism than they have thus far, not to imagine that the information contained at Seeking Alpha has been conclusively proven or that—as the 2016 report is at great pains to underscore is not the case—we can be certain whether any of the activities described in it are illegal or otherwise illicit.

With all that said, here’s what we learn from a major report on Axos published years before America realized it was the lender that has saved the Trumps from financial and political ruin again and again during Donald Trump’s ongoing political career:

The report goes on to exhaustively substantiate its allegations in links to public records and in many cases through actual images of those records.

Proof has previously expressed its concern, in reaction to the aforementioned Axos Whistleblower Case, that Trump’s new lender has a long history, via his involvement with Axos as its largest investor, with a digital operation that not only is the “lender of last resort” for the Trumps but also one that specifically does business with (a) foreign criminals, and (b) former leaders or public figures in three nations that Trump has attempted to collude with during his brief time as a politician in the United States: Russia, China, and Venezuela (as well as Kremlin assets in Ukraine, as discussed at great length in the 2020 national bestseller from the Proof Trilogy, Proof of Corruption).

The Seeking Alpha Report confirms Axos’s connections to all these countries in deals that look problematic on their face and consistent with the Axos Whistleblower Case.

Worse still, the Seeking Alpha Report limited itself almost entirely to deals done by Axos in one particular state: Florida, which has been Donald Trump’s home for years.

This nexus of a Don Hankey-funded operation, the Trump Family’s borrowing history, the State of Florida, and possible deals with criminals in Russia, Venezuela and China is genuinely terrifying in light of all the ways the Knight Bond is irregular and in view of all of the secrecy that still surrounds it.

With this in mind, Proof here itemizes, for free for the general public, the ways we’ve learned in just the last 72 hours that everything we were told about the Knight Bond was apparently a lie.

First, however, here’s an overview of the well-source coverage of this topic Proof has already offered (with links to each report, most of which contain free Introductions):

Bibliography: Every Proof Report on the Ongoing Trump Bond Scandal

(in chronological order, with each Proof report’s visual “color code,” title, and permalink)

The Trump Bond Crisis: The March 11, 2024 Bond

#01 | 🟥 | “Source of the Money for $91 Million Bond in Trump’s Defamation and Rape Case Appears to Have Major Kremlin Ties” (link)

#02 | 🟦 | “The New Questions Federal Investigators Must Ask on An Emergency Basis About Trump’s Eleventh-Hour Bond Proposal—Whose Apparent Kremlin Connections Increase By the Hour” (link)

#03 | 🟩 | “Experts Said for Weeks That Trump Might Get Bonded By Kremlin Allies. Now It’s Happening—Causing a National Security Crisis—So Why Is Media So Silent About the Greenberg Family?” (link)

#04 | 🟨 | “Trump, Zuckerberg, Musk, Greenberg, Yass, TikTok—Dozens of Far-Flung Narratives Are Suddenly Coming Together As Trump Seeks a New Surety Bond to Avoid Ruin” (link)

#05 | 🟧 | “Everything You Need to Know About Donald Trump’s Impending Financial Ruin As a Hard $454 Million Bond Deadline Arrives Monday” (link)

#06 | ⬜️ | “It Sure Looks Like the Chinese Communist Party Is Trying to Bail Out Donald Trump in Advance of His Monday Bond Deadline” (link)

The Trump Bond War: The April 1, 2024 Bond

#07 | 🟪 | “New Evidence Suggests That Donald Trump’s $175 Million Bond May Be Every Bit As Dodgy As Almost Every U.S. National Security Expert Feared” (link)

#08 | 🟫 | “The Story of How Donald Trump Secured His Eleventh-Hour $175 Million Bond Is Already Changing Dramatically—Probably Because None of It Appears to Be True” (link)

#09 | ⬛️ | “Inside Trump’s Bond War” (link)

#10 | 🔲 | “Everything We Were Told About the $175 Million Bond Donald Trump Got Was a Lie” (see below)

To gain instant access to the above reports in the “Trump Bond Crisis” series, click this button:

Keep in mind that the list of public deceptions that follows is non-exhaustive, as it focuses exclusively on what we’ve learned in just the last 72 hours. A comprehensive accounting of the problems with the Knight Bond is to be found in the nine Proof reports above, which are hereby explicitly incorporated into the Proof report below.

Note that, just like the Seeking Alpha Report that this Proof report links to above, “This article does not mean to allege or imply that any unconvicted individuals discussed herein have engaged in any illegal acts.” That will be a determination for, as appropriate, federal investigators and/or state and federal courts, beginning with Judge Engoron’s court in New York later this month.

Proof will cover Trump’s April 22 hearing when it occurs. The ex-president himself won’t be present at the show-cause hearing, as he’ll still be in his criminal trial—in another courtroom in the city—facing 34 felonies for Falsifying Business Records.

(While PBS reports that defendants in New York are rarely sentenced to prison for FBR charges alone, it’s not wholly unheard of, and remains a possibility in Trump’s case.)

The Top 10 Ways in Which Everything That We Were Told About the $175 Million Bond Donald Trump Got Was a Lie

(1) The Bond Fee

Hankey, Trump’s new lender, first said that he dealt with Trump the way he would anyone else, which—if true—would mean he charged Trump a usurious rate for his bond. As Proof has reported, Hankey’s current average interest rate for loans to poor people and military veterans is 19% interest; translated to a bond, that’d mean a 19% fee for Trump’s bond as opposed to the usual (at least according to Reuters, but see below for more) 1.5% fee. In other words, about $33.3 million instead of $2.5 million.

But then Hankey changed his tune.

In the face of ever-increasing questions from reporters about the terms of his bond deal with Trump—which terms Hankey wouldn’t reveal—the CEO of Knight Specialty Insurance Company, an avid Trump fan and voter and donor by his own admission, switched to a second, quite different line about the fee that he charged Trump, calling it “modest.”

But then Hankey changed his tune again.

Once he became aware that he was going to have to reveal the terms of his deal with Trump at the April 22 show-cause hearing just forced upon him—and Trump—by a filing from the New York Attorney General’s Office, which objected to the so-called Knight Bond on at least three distinct grounds, including Knight’s capitalization level and its eligibility to do any surety work at all in the State of New York, Don Hankey offered a third take on how to classify the fee he’d charged Donald Trump for his bond.

Now Hankey confessed to the American public that the fee was “low.”

Moreover, Hankey admitted that he had set the fee “low” because he believed that the transaction was “low risk”—though he was in fact lending to a man considered such a high risk as a borrower that no bank worldwide will led to him anymore.

But now that Hankey has been caught giving a sweetheart deal to a confirmed rapist and career con man, not to mention a current multistate defendant facing 88 state and federal felonies in four U.S. jurisdictions, he’s yet again changed his tune in a recently released confession. As he told Reuters, it’s not his fault that after decades in lending he made a terrible business decision in the bond fee he set for Trump, as he (emphasis supplied) “now feels [he] did not charge Donald Trump enough because of New York Attorney General Letitia James’ subsequent scrutiny of the bond…[and] the media attention around it.”

In other words, Hankey claims he didn’t realize he’d made a bad business decision in the industry he’s worked in for decades until every entity in the United States that could possibly weigh in on the decision—from government to fellow businessmen—confirmed for him that he’d done so. That’s an extremely hard explanation to credit.

Even worse than this, however, Hankey now seems to admit that he set his bond fee so far below market rate—which could make his deal with Trump an illegal campaign contribution—that his belated realization that he had done this (which realization he indicates was prompted by him “getting a lot of emails, a lot of phone calls”) “Maybe is part of the reason [Trump] had trouble with other insurance companies.” That is, Hankey here surmises that other insurance companies were looking for a 1.5% bond fee and Trump was either unwilling or unable to pay a $2.5 million bond fee (despite saying in a sworn deposition last year that he had $400 million available for any civil suit against him) and therefore couldn’t reach a deal with any other lender worldwide.

{Note: Trump’s perjurious lie about his liquid assets is a further deception that this report isn’t explicitly itemizing in this list because it’s already been discussed at great length in this series.}

(2) The Location of the Collateral

First Don Hankey said that Donald Trump had “kept” all of the cash collateral he had used to secure his bond, meaning that it was (a) wholly under Mr. Trump’s control, (b) inaccessible to Mr. Hankey, and (c) a cache of funds Trump could still earn interest on.

Now Don Hankey says—without clarifying whether he gave bad information at first or whether the actual terms of his deal with Trump changed once the two men knew it would be coming under judicial and law-enforcement scrutiny—that “the cash is held at a brokerage firm and pledged to Knight, and that Knight can access it if needed.”

So either Hankey lied at first, is lying now, or changed his conduct between his first and most recent statements in order to protect himself from any blowback that could arise from a state-court review of his transaction with Trump.

(3) The Source of the Collateral

First Don Hankey said he didn’t know for certain the source of the cash collateral but believed it had all come from Trump. That would have made sense, of course, as the RNC has been very clear in saying that it won’t help Trump with his legal costs, and Trump, for his part, has been very clear in saying that he has enough money to pay his legal bills without help from the RNC. It would be a humiliating state of affairs for Trump if it were to be revealed that as a self-professed “billionaire” he doesn’t even have the money for a 1.5% fee on an already-reduced appellate bond (the bond was first $454 million, then it was dropped to $175 million by a New York appeals court).

Now Hankey is hedging his bets about where Trump got the money for his collateral, saying, “I don”t know if it came from Donald Trump or from Trump and supporters.”

It certainly seems like Hankey has caught wind of the fact that Trump did not have the $400 million available for cash collateral that he (and Forbes, and the New York Times) have been reporting he did—even as every Trump biographer, including this author, was consistently saying otherwise—and that he feels he must now get ahead of that revelation in advance of Trump’s destitute condition being likely to come before the court and plaintiff (Judge Engoron and Attorney General Letitia James) on April 22.

(4) Trump’s Liquid-Asset Reserves

As noted above, Trump has been clear on the size of his liquid asset cache—or rather, has been clear on what he wanted the public to believe. But apparently he told Hankey the truth, or at least something closer to the truth, as now Hankey is revealing it to the public to (one presumes) preserve whatever scrap of decency and shred of his prior reputation he can by implying that he did due diligence before lending to Mr. Trump.

Here’s what Hankey is now telling Reuters:

Given that Hankey now says that even the $175 million in cash collateral Trump put up may not have come from him, there’s no way to know if Trump has any liquid-asset reserves at all. Certainly, Hankey is positioning himself to try to be on the right side of history by revealing that Trump was lying in his 2023 depo (as well as a more recent statement about having $500 million in liquid assets) before Trump himself is caught out in this brazen lie in court.

It may in fact be the case, as this author has surmised, that Trump has as little as $10 million to $25 million available to put toward a cash-collateral sum, and may not have been willing to put up that amount himself because it’s all he has to live on (which of course seems like quite a lot to live on, until we remember that Trump has claimed to be worth $10 billion—not $10 million, but $10 billion).

(5) The Typical Cost of a Bond

Reuters reported that bond fees are usually 1% to 2% of the face value of a bond, which was news to this former criminal defense attorney—in whose experience bond fees are almost always around 10% of the face value of a bond—but that reporting has now taken hold in the imagination of many who’ve been following the Trump Bond Crisis.

Which is why I was relieved to read this Newsweek report, which quotes online agency Insureon, “which handles small-business insurance”, as stating that “a surety bond’s fee can range from 1% to 15% of the total bond amount.”

In other words, while Reuters and some other outlets may be doing Trump a solid by stating that an appropriate fee for his bond—the amount a party being bonded doesn’t get back—would be around $2.5 million (meaning that as long as Hankey charged Trump around that amount, the fee was reasonable and the deal itself not a campaign finance violation) Insureon and others, such as this author, are saying that a bond fee in this case could easily have been as high as $25 million.

In noting this, Proof is mindful of the fact that everything about Mr. Trump’s situation would have militated for the highest end of any bond price range: (1) Don Hankey knew Trump had no other options, because no one else would lend to him (as he admitted in court); (2) Hankey knows Trump has a history of lying to, cheating, and even trying to destroy his lenders, making it a big risk to be associated with him as a lender to any degree ; and (3) Hankey knows Trump is financially destitute due to his bond in the Carroll I case, his bond in the Carroll II case, the civil judgment just issued against him in England for frivilously suing Christopher Steele, the fact that he can’t afford to pay his attorneys himself, the fact that Hankey knew (even when the general public didn’t) that Trump had lied under oath about his liquid assets, and so on.

These factors and others would have made the actual “market rate” for a bond fee in this case much closer to $25 million than $2.5 million, and of course even higher than $25 million if Hankey was in fact as committed as he claimed he was to being as exploitative of Donald Trump as he habitually is of poor persons and military veterans.

(6) Whether Don Hankey Handled the Deal in the Normal Course of Business

In his first five to ten interviews about the Knight Bond, Hankey maintained a single unwavering line: what he did for Trump he would have done for anyone; the deal was finalized quickly and with ease; the deal terms were normal under the circumstances, meaning they were the same terms he would give to anyone anywhere on these facts; and he believed there to be low risk in participating in this transaction with Trump.

Would you be surprised to hear that Hankey has changed his tune on this as well now that he knows the whole country will find out what he charged Trump for a bond fee?

According to this Newsweek report, Hankey now says that “We [Knight Specialty Insurance Company] probably didn’t charge [Trump] enough [for the bond fee].”

This suggests that, when that fee is revealed on April 22—if not before—it will be well under $2.5 million rather than the $25 million or above it could have and perhaps should have been, and since bond fees are non-refundable purchases, what Hankey did was probably more like give Donald Trump a campaign donation of $20+ million than merely a run-of-the-mill bond he would have given to anyone.

Proof leaves the determination of whether any campaign finance crimes have occurred here to the New York Attorney General’s Office, of course, but suffice to say that with his sudden change in tune on the above items there are some early indications that Hankey is concerned—not just about the public but law enforcement seeing, in all its ugly spectacle, exactly what he did for Trump to save him from financial and political ruin (having already been given credit, by the Washington Post, for enabling Trump’s 2024 presidential campaign in the first instance through his lending largesse).

(7) The Feasbility of Donald Trump Making a $454 Million Bond

ProPublica has now picked up the exclusive Proof reporting from several days ago about Trump and his legal team having hidden from both the trial and appellate courts in New York that “several days” before the Monday, March 25, 2024 ruling that lowered Trump’s bond from $454 million to $175 million—a reduction issued on the grounds that, as Trump had represented to both courts, no one would give him a $454 million bond and indeed such a bond was a “practical impossibility” for anyone in real estate—he was told by Hankey that Hankey would give him a $454 million bond.

This means much more than that Trump and his attorneys simply committed a fraud on the courts of New York: it means, arguably, that the bond reduction itself should be expunged from the record—on the grounds that it was achieved via a misrepresentation to the court—and that, in consequence, Hankey and Trump should have to go forward with the $454 million bond they’d agreed upon in principle days before it was lowered.

{Note: Unless Hankey now wants to back out of that deal, which would be understandable.}

At a minimum, the appellate court should receive a Motion to Reconsider from the New York Attorney General’s Office on the basis of this new information, so that the court can decide if it would have come to the same conclusion about the bond knowing the information that Donald Trump and/or his legal team was hiding from it at the time.

While it’s possible that this was not an intentional fraud on the court—for instance, Trump may have connived to hide from certain of his lawyers that he’d indeed found a lender on his $454 million bond—but even if Trump’s attorneys found out what had happened after the fact (that is, after they had submitted their appeal of the bond) they had an unambiguous duty to correct the record that they didn’t honor, which breach would still likely constitute an ethical violation per conventional state bar guidelines.

(8) The Feasibility of Donald Trump Using Real Estate As Collateral

Trump technically made two false submissions to the trial and appellate courts: the first was about whether lenders would touch a $454 million bond generally—Trump and his son Eric Trump went on media saying that lenders wouldn’t touch more than a $100 million bond in circumstances like this—but the second was about whether any bank would take real estate from Trump as collateral for his bond.

Trump insisted that none would.

We now know that that, too, was a lie.

ProPublica reports that, as Proof had surmised by process of elimination previously, “billionaire California financier Don Hankey said he reached out to Trump’s camp several days before the bond was lowered, expressing willingness to…use real estate as collateral.”

(9) Whether the Deal Was “Easy” for Knight to Handle Financially

Proof can’t count how many times Hankey told U.S. media that the deal was “easy” for him to agree to because the bond amount was “relatively low”—and it can’t count the number of times Hankey said this because it appears that he said it to every journalist he spoke to. He even left the impression, given his story of reaching out to aid Trump when the bond was still at $454 million, that—while obviously a heavier lift—even the $454 million bond was readily doable for his company and not a prospect he felt much trepidation over.

But now Hankey has changed his tune on this point as well, telling ProPublica that “making a deal [with Trump on the $454 million bond] would have been ‘difficult.’”

It’s important for readers to understand here not merely that Hankey is changing his tune but also why he is doing so.

If Trump’s legal team knew Hankey was prepared to cut a deal on a $454 million bond before the appeals court in New York dropped the bond to $175, then yes, it made a material representation to the New York courts that’s a serious ethical violation in the legal profession. But even if Trump’s legal team learned Hankey was prepared to cut a deal on a $454 million bond after its last filing with the appeals court in New York before that court dropped the bond amount to $175, as noted above Trump’s lawyers would have had a duty to correct their prior filing. Their failure to do so would breach their duty to the court as (to use a bar term) “officers of the court”, a serious ethical violation in the legal profession. So what does this have to do with Hankey changing his tune on this point in particular?

A lot.

The reason it’s vital that Hankey called back ProPublica to change his story yet again and say that really the $454 million would have been hard for him to do—and yes, he actually thought about what he had told the digital publication the first time and then called back to offer a new story—is because Hankey now needs to exculpate Trump and his attorneys from getting into serious trouble with the court (or, as to Trump’s attorneys, with the state bar).

Hankey’s reasoning appears to be that if he never really said to Donald Trump or to his attorneys that $454 million was eminently doable, they didn’t really have to correct the record they had made in filings with the court(s), and therefore the courts don’t really have cause to bump the bond back up to $454 million due to any misrepresentations or failures to correct the record for which Trump and/or his legal team are responsible.

So Hankey is at once protecting himself—because he much prefers the Knight Bond at $175 million rather than $454 million—while also protecting Trump and his lawyers.

(10) Whether Politics Came Into Play As GOP Megadonor Hankey Decided to Rescue Trump From Financial Ruin

They obviously did. But until now, Hankey not only hadn’t acknowledged that but had repeatedly said the opposite, insisting he was making a business decision and would have made the same decision in any situation with any prospective client—including a Democratic politician. All of that is obvious nonsense, of course, but he did say it.

Now we know just how untrue it was.

According to Hankey now, prior to contacting Trump’s legal team he was obsessed with how unfairly he believed Trump was being treated—a political judgment, in context, given that every mainstream legal analyst I’ve read (and I include my own judgment in this) is that Trump has received special beneficial treatment in NYC, if anything.

Hankey has a different view—one clearly guided by partisanship, not legal expertise.

He thought Trump acted reasonably with his lenders and the federal government on his taxes; he thought Judge Engoron had set too high a civil penalty in the case; he was “confused” about why “other[ ] [lenders] would have rejected [Trump]”, though of course even as much due diligence as a Google search would have revealed exactly why lenders had stopped working with Trump. And he decided that he had to help Trump because clearly other lenders were being political in a left-leaning direction, or, as he put it, “If you’re a public company, maybe you don’t want to offend [the] 45% of the population [that opposes] Trump.”

Even this last statement is political, of course, as it sees Hankey fancifully pretending that a man who’s had a well over 50% unfavorability rating since January 6, 2021 in fact has a favorability rating that’s at least 55%. Once again, a simple Google search would have disabused Hankey of his convenient fabulism, and so would have eviscerated his politically motivated self-justification for lending to Trump (as his basis for deciding Trump was being mistreated had been invented). But even putting this aside, in order for Hankey to talk himself into his loan being “more of a business decision” when it clearly wasn’t, he had to deem himself better on the law than a judge, more familiar with civil statutes than the New York Attorney General, a better pollster than any professional American pollster, and a smarter banker than any banker in the world.

In other words, yes, it was a political decision—not a business judgment—that Hankey made. And no one he wasn’t voting for and donating to would have gotten his largesse.

Conclusion

To repeat what this report indicated in its Introduction, the above list of deceptions is non-exhaustive, as it focuses exclusively on what we’ve learned in just the last 72 hours.

What I suspect many Proof readers who have read all ten Proof reports on the Trump Bond Crisis (now the Trump Bond War) are now thinking is this: imagine what would have happened if major media had put the kind of effort into investigating the Chubb Bond (the one Trump posted on March, 2024 in the Carroll II case) that it’s starting to put into investigating the Knight Bond!

And in the view of Proof, that’s exactly the right way to think about all this.

There’s no reason to think the Chubb Bond was any less the product of a spectacular web of deceit than we now know the Knight Bond was. And we long ago learned that Donald Trump can’t be adequately covered using conventional reportage; curatorial journalism that draws from hundreds of media outlets and sources from around the world and looks to both the present and the past is required to adequately frame in American history, current geopolitical context, and conventional legal practice exactly why Trump is so dangerous a law-breaker.

We can even look at what smart, well-informed social media users are now saying on this subject for yet another indication of how inadequately incredulous major media has thus far been in reporting on the Trump Bond Crisis and the Trump Bond War.

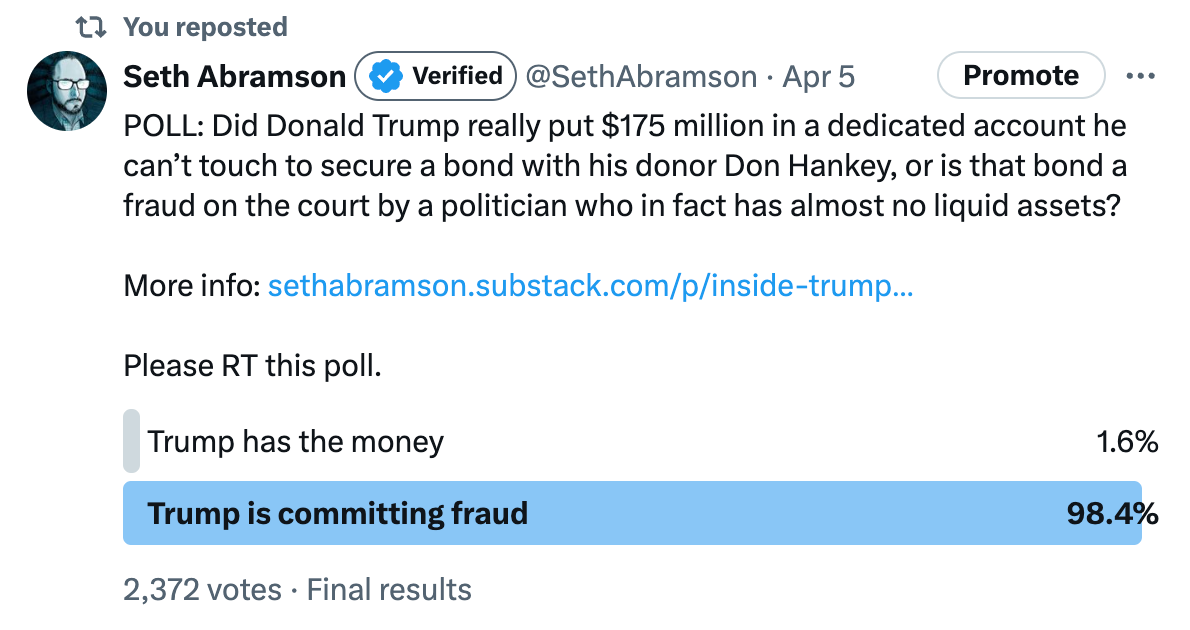

Accepting that Proof readers, including those on social media, do lean progressive—while also being fair-minded and extremely well-informed—Proof asked the same question of its readers on both Threads and Twitter: “Did Donald Trump really put $175 million in a dedicated account he can’t touch to secure a bond with his donor Don Hankey, or is that bond a fraud on the court by a politician who in fact has almost no liquid assets?”

Here are the unscientific results of those two polls:

Threads

In total, over 4,250 votes were cast, and between 97% and 98% of voters said that they think Trump was and is committing fraud with the Knight Bond. While certainly that figure would be far lower amongst a more centrist group, we cannot imagine it would dip below 60% given Trump’s demonstrated history of fraud, with even conservative publication The Hill observing that Trump has been “a financial fraud for decades.”

And indeed the general consensus across all of social media—in all corners but those inhabited by MAGAs, that is—appears to be that the Knight Bond is extremely dodgy.

And it is.

But so was the Chubb Bond—whose peculiarities major media ignored rather than alerting American news consumers (and, as importantly, voters) to their existence.

Meanwhile, Proof wrote six full-length reports on how extremely dodgy it was, all of which are included in the Bibliography above.

Arguably, major media still has a chance to right its past errors and return to the Chubb Bond that Proof covered so comprehensively, knowing what it knows now.

Will it? Who knows.

But all the assessments now being applied to the Knight Bond can equally be applied to the Chubb Bond, and then some. Here’s hoping media gets itself together and starts doing its job.

If you’re interested in reading more research and writing from Seth Abramson, you can check out his Top 20 History substack, Retro, by entering your email address in the space below:

If someone, like Hankey, doesn’t know that everything the orange fascist prick touches, dies, deserves what he gets or won’t get, which is a damn dime, from the lying SOB. Hankey is a fool.

OFP lies as easily as he breathes, it’s absurd anyone can believe him about anything.

The fraudster obtains a court ordered bond, for a conviction of fraud, under fraudulent means- who woulda thunk. FFS.

I’m always worn out after reading your reports, but appreciate them very much.

2 more weeks of uncertainty AND of time for ‘media’ to step up to their duty. So far every time one hopes now trump will be caught, he has escaped. It must stop, this escaping justice!